Wolf Money(portfolio update for end July 2023)early

A reminder of the Singapore Miracle

Happy Birthday to my beloved country, Singapore, a place where I call home. If Singapore was a listed company which could be bought and sold like any other securities on the stock exchange, the “Singapore stock” would have made you close to 159x return in 58years. Singapore GDP per capita started at a mere USD $500 in 1965 had risen to USD $82,000 by end of 2022. On Aug 9th 1965, a country barely half the size of London with no natural resources and 2m population comprised of mostly the poor and the hungry set out to be a new Nation with huge odd stacked against her. Our pioneer generation was given the daunting task of undertaking Project Singapore, creating jobs and attracting investments into our country. With sheer luck and ingenuity, a miracle of atomic proportion was born out of wedlock. Once again here to the Grand Old Lady, Happy 58th National Day, Singapore! 🥂

Mental Wellness

Coco Lee’s sudden death shocked the world of entertainment. A seemingly joyful lady resorting to killing herself is a growing trend of mental health related suicides among celebrities.

In Singapore, one research shown 13% of our population suffers from some form of mental illnesses and our suicide rate had reached a 22 years high with a growing number of youths choosing to end their life prematurely. Given financial, relationship and work related stress showing an alarming increase in Singapore, we as brothers, sister, husband, wife, father, mother, son, daughter and friend of our loved one should double down our effort to support and help those around us who are showing signs of extreme stress. I, unfortunately lost a friend whom I care and respect dearly to the same circumstances. The incident left an indelible mark on me and changes my prospective about life forever. Life is short, be happy. Sometime I asked myself if I had been more attentive, showing more care and concern, things might have been different. A call or a simple text message showing concern might be the fine line of saving one’s life or losing the person forever. Given the ever increasing financial burden and societal pressure, mental health is under full assault.

In western society, mental disorder is considered a common illness but in Asian context we don’t usually talk about it openly and it is not always clearly defined due to the lack of knowledge and the stigma surrounding the topic on mental health. Everyone should take a proactive approach to improve mental wellness, seek professional help if needed. Mental illness like any other illnesses could be treated and cured if detected early. A call to action is needed to tackle the problem. Another life loss to mental disorder is one loss too many. God Bless everyone with great mental well-being.

Samaritans of Singapore (SOS) Hotline 1767 WhatsApp 915 11767

Lone Wolf Fund(LWF)

Portfolio as at end of July

1.) Cash

2.) Yangzijiang Financial Holdings(YZJFH)

Commentary

The Singapore market as usual was suffering from its own chronic and structural weakness. Another weak July month given the exceptionally bullish performance from Wall Street. STI Index had just managed to turn positive for the year. LWF was up by 1.5% for the month, YTD gain stands at 6.5% (excluding dividend and cash yield). Lone Wolf Fund still managed to eat out a gain help by Boustead Singapore even after HPC losses and BOC going XD.

I had sold my holding in Bank of China(BOC) and taken some profit off the table. The sale was technical. The weakness in BOC was due to Goldman Sach downgrading the Chinese banking sector. I had taken dividend and capital gain in excess of 10% from the sale, it would be another year before BOC shareholders see another dividend payout. I used some of the profit from BOC to clean up the portfolio with the sale of underperforming Haw Par Corp. HPC seem to be suffering from the lack of interest and it remains one of the most undervalued stock listed on SGX.

I am raising capital just in case there is an opportunity for me to buy into “another of my many potential distraction”. I am still sitting on the fence whether the current price of that one particular “distraction” make sense in the current market condition. I am not under pressure to do anything with the proceeds from my recent sale. Patience is the name of the game.

To be honest, I am confused by the market direction, most indicators are flashing red or at least flashing orange but that doesn't mean the market can’t go higher. Market can stay elevated longer than an individual could stay solvent. Greed and fear index had reached the highest point of the year. An index point higher than 75 had always follow by a sharp change in market sentiment that led to a market correction.

There was news on SingPost doing a strategic review. Imho It was a long time coming. Government is open to SingPost raising domestic postage fee, it is a far superior plan than tax payer taking over the money losing baby. For the review, the last thing SingPost want to do is to sell away SingPost Centre Mall for quick gain which is critical to SingPost profitability. There might be quick gain but it might be hard to replace the huge rental income that keep SingPost afloat. Anyway I am just Kaypoh, it is up to SingPost shareholders to decide. Sembcorp had decided to call off the sale of their waste management unit, it is definitely good news for most households, as the would be acquirer is likely to raise fees for waste disposal. The middle option for Sembwaste is to seek a listing in our stock market, giving a shot in the arm for our struggling market.

I like the market to go higher since I am still vested in the market. The cautious side of me is asking me to take a more defensive position in preparation for the next downturn which can be anytime within the next 12 months. My gut feeling which maybe wrong, we are somewhere similar in 2006-2007 where market are chucking along nicely before the big downturn in 2008.

Cash

With rising cash, I took the opportunity to apply for more SSBs. 2.99% for 10 years is decent yield to house some temporary cash. Rest of the capital is sitting in a high interest account.

Boustead Singapore

I enjoyed reading both copies of Boustead S’pore and Projects annual report. There are some nuggets of important informations in the annual report. For example, the 21% increased in stake of Boustead Projects by BSL had not factor into last year earning of BSL. Base on last year earning, an increased of 21% in BPL shareholding would have increased the earning by $3.9m excluding any additional one time negative goodwill gain of $25m for acquiring BPL at below book value(balance sheet item). Shares continued to trade firmer, the market might be realising the potential earning growth of the company in the next few years.

The 156 rooms Como Metropolitan Hotel Singapore at 30 Bideford will be opening its doors for guests from 1st of September 2023. It will contribute to Boustead Singapore earnings from 2H24. The timing of the opening is impeccable given the host of events and concerts held in Singapore over the next 9 months. Cold play and Taylor Swift each drawing an estimated crowd of 300,000 with many coming from neighbouring Southeast Asia countries. Other act like Sam Smith is likely to draw capacity crowd. Demand for hotel rooms will be sky high especially in Orchard area. Hotel room rate starts at $625 for a Cairnhill Room to $1080 for a Como Suites. Gross revenue generated for the hotel alone can potentially be up to $30m yearly if I take average room rate at $650 x 365 days x 80% occupancy. As for the other leasable space in Bideford, 76% or 3 out of 4 floors of retail, offices and medical suites had been taken up. I estimate the property alone can potentially contribute earning up to 2c per share on a steady state basis. Share of Boustead Singapore is trading at CD with dividend of 2.5c paying out in August. There was good news on geospatial front this week, the company announced a multi-year contact win worth AUD $48m to provide Esri ArcGIS system and support to the Australian Federal Government. The contract win will have a positive impact for FY2024 result.

Yangzijiang Financial Holdings(situational) (YZJFH)

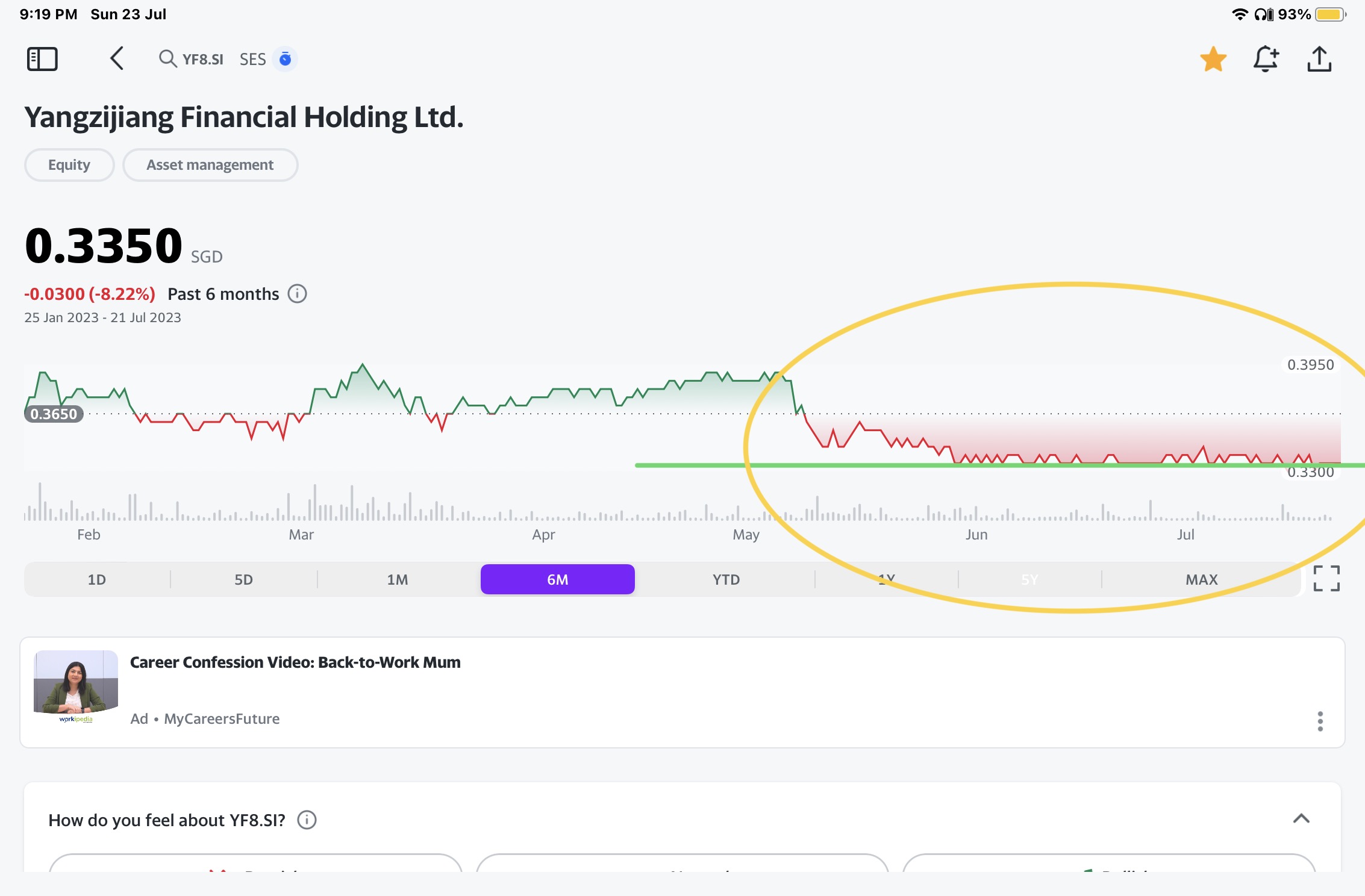

In typical Lone Wolf fashion, I am back bargain hunting. YZJFH’s share price had been cut by half since March last year. To be frank, I didn’t see this purchase coming. I usually don’t buy into Singapore listed Chinese company but given the proven track record of Mr. Ren at Yangzijiang Shipbuilding, I am willing to give it a taste(you know like an entrée, just to warm the stomach). With more than 3/4 of the board members being Singaporean, it does give an impression of better corporate governance. Base on my initial research, YZJFH look like an undervalued company. Share is trading at 1/3 book value and a historical p/e of less than 8x with the potential to half their p/e in FY2023 if they can find enough mojo to recover from last year poor result. The company is in a net cash position. Last year result contained a big write off of $136m due to non performing loan that caused earning to drop by half. Base on my initial understanding of their business, they try to be in similar business model like BlackRock by being a multi assets and multi disciplines fund manager. They managed their own capital and capital from exterior party with some coming from wealthy Chinese family offices. Family offices in Singapore had grown from 100 in 2017 to 700 with half of the total Asian family offices base out of Singapore. YZJFH might be the closest to a family office play. Recently they were entrusted with $500m by a family office. I will be looking at their first half number coming Aug to see where they go from there. The company has a 40% dividend payout ratio which can potentially raise the dividend yield to 8% if the earning recovered this year. The position is too small for me to do a full write up. Stock is near 52 weeks low with very tight trading range of between 32c to 34c since June(yellow circle). The company had spent close to $112m doing share buyback since June last year, buying close to 8% of the outstanding share without reply to the share price.

Key risks involved the robustness of their loan book and currency risk as RMB had slide 4% against Singapore dollars since the start of this year as most of their asset(87%) are held in RMB. The skill of the fund manager plays an important part too when investing in the company. The spinoff from Yangzijiang Shipbuilding last year coincided with a huge drop in profitability didn’t bode well with many investors, hopefully 1H FY2023 numbers can regained some of that lost confidence. The small position is to keep myself curious with the company latest development.

Please consider following us on telegram for the latest update on Lone Wolf investor by clicking on the link below. No form filling, no payment required, no collection of data, no data mining, no hard selling, no obligation.

https://t.me/joinchat/oCgkD3sQFRMzMWM1

Disclaimers

All investments is highly speculative in nature and involves substantial risk of loss. We encourage our reader to invest very carefully. We also encourage reader to get personal advice from your professional investment advisor and to make independent investigations before acting on information that we publish. Much of our information is derived directly from information published by companies or submitted to governmental agencies on which we believe are reliable but are without our independent verification. Therefore, we cannot assure you that the information is accurate or complete. We do not in any way whatsoever warrant or guarantee the success of any action you take in reliance on our statements. All information provided are for education only. Buyer beware,do you own due diligence

Comments

Post a Comment